P2P payment scams: when 'sent in error' is a scam

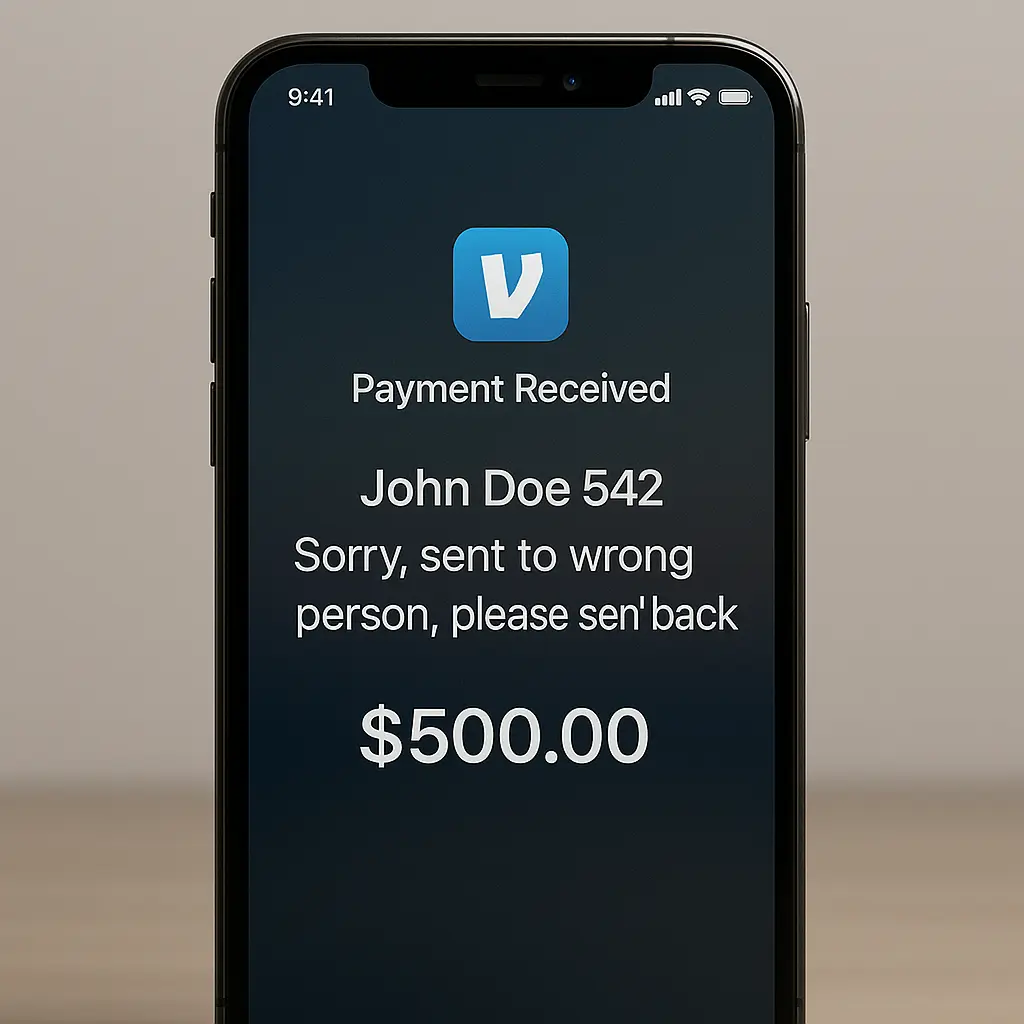

You wake up to a notification. Someone sent you $500 on Venmo. You don't recognize the name. A minute later, a message arrives: "Sorry, I sent that to the wrong person. Can you send it back?"

It feels harmless. Maybe even like the right thing to do. You send the money back. Two days later, the original $500 disappears from your account. The platform reversed it. But the money you sent? That's gone. Your account is now negative $500, and the platform expects you to cover it.

This is the "accidental payment" scam. It works because it flips the script. Most scams ask you to send money. This one starts by sending you money. That reversal of expectations disarms your skepticism. You think you're helping someone fix a mistake. You're actually funding a fraud.

Here's how the scam works, why payment platforms struggle to stop it, and what to do when an unexpected payment lands in your account.

The mechanism: fake money in, real money out

The scam operates on a timing gap. Payment platforms process transfers quickly, but they verify funding sources slowly. That delay creates a window where money appears in your account before the platform realizes the payment method was fraudulent.

The scammer sends you money using a stolen credit card, a compromised bank account, or a payment method they've already reported as unauthorized. The platform processes the transfer immediately. You see the funds. The scammer messages you claiming they sent it by mistake. You send your own money back using your own legitimate payment method.

Days or weeks later, the platform completes its verification. The original payment gets flagged as fraudulent and reversed. The money disappears from your account. But you already sent your money to the scammer using a legitimate transfer that won't be reversed. The platform holds you responsible for the negative balance.

The FTC warns about payment app scams that exploit this gap. Scammers know platforms prioritize speed over verification at the point of transfer. They use that window to create the illusion of a mistake.

The scam works because your response feels reasonable. Someone made an error. You're correcting it. But the error is fabricated. The payment you received was never real money. The payment you sent was.

Variation one: the business account excuse

Some versions of this scam add a layer of urgency by claiming the sender used a business account and needs the money back immediately to avoid fees or complications.

The message might say: "I sent this from my business account by mistake. If I don't get it back today, my accountant will flag it as fraud and I'll have to file a dispute. Can you just send it back real quick?"

This variation works because it introduces a deadline and appeals to your desire to help someone avoid bureaucratic hassle. The scammer is betting you'll act fast to prevent their supposed problem rather than pause to verify the situation.

The business account claim is almost always false. Scammers don't have business accounts. They're using stolen credentials or fraudulent payment methods. The urgency is manufactured to prevent you from contacting the platform or thinking through the situation.

If someone claims they sent money from a business account by mistake, that's a stronger signal to stop and verify. Legitimate businesses have accounting processes that don't rely on strangers sending money back through peer-to-peer apps. They contact the platform. They don't message random users.

Variation two: the overpayment setup

Another version involves a purchase or service. Someone contacts you about buying something you listed online or hiring you for a gig. They send you a payment that's larger than the agreed amount. Then they ask you to refund the difference.

The message might say: "I accidentally sent you $800 instead of $300 for the couch. Can you send back the extra $500? I already submitted the payment and can't cancel it."

This version works because it frames the refund as part of a transaction you initiated. You listed the couch. They responded. The overpayment feels like an honest mistake in the context of a real sale. You send back the difference. Then the original payment reverses, and you've lost the $500 you refunded plus the item if you already shipped it.

The FBI's Internet Crime Complaint Center tracks overpayment scams as a persistent fraud pattern. The 2023 report showed these scams cost victims tens of millions annually, with payment apps increasingly used as the mechanism.

The overpayment setup works particularly well on platforms like Facebook Marketplace, Craigslist, and OfferUp, where people expect to handle transactions directly with buyers. The scammer blends into the normal flow of selling online. The request to refund the difference feels like a reasonable fix to a payment error.

If someone overpays and asks for a refund, stop. Don't send anything back. Contact the platform. Let them reverse the entire transaction. A legitimate buyer who overpaid will understand that you need to verify the situation before sending money.

Why payment platforms can't fully prevent this

Venmo, Zelle, and Cash App all have fraud detection systems. They scan for stolen credentials, unusual transaction patterns, and known scam behaviors. But they face a structural problem: they're designed for speed. Verifying every funding source before processing a transfer would slow the service to the point where users would leave for faster competitors.

The platforms prioritize user experience. Transfers happen in seconds. That speed is the product. But speed requires processing payments before full verification completes. That gap is what scammers exploit.

Zelle operates differently from Venmo and Cash App because it's integrated directly with banks. Transfers through Zelle are nearly instant and often irreversible, which makes the scam more damaging when it succeeds. If you send money back through Zelle, the platform has fewer tools to recover it. The Consumer Financial Protection Bureau has documented cases where Zelle users lost thousands because the platform's reversal process is limited compared to card-based services.

Venmo and Cash App offer slightly more protection because they're not bank-to-bank transfers. The platforms can freeze accounts, reverse transactions, and investigate fraud. But those protections activate after the fact. They don't stop the scam at the moment of contact.

The platforms also face a detection problem. The initial transfer looks legitimate. Someone sent you money. That's not inherently suspicious. The scam only becomes visible when you send money back, and by then, the scammer has what they wanted. Automated systems struggle to distinguish between a scam and a legitimate correction of a genuine mistake.

Some platforms have started adding warnings when you receive money from an unfamiliar account or when someone asks you to send money shortly after receiving a payment. Those warnings help, but they rely on you reading and heeding them. Scammers count on urgency and social pressure to override caution.

The psychology: why this scam works

The "sent in error" scam succeeds because it reverses the usual fraud dynamic. Most scams ask you to send money to a stranger. This one starts with a stranger sending money to you. That inversion disarms skepticism.

Receiving money feels like proof of legitimacy. If someone is willing to send you funds, they must be real. They must be trustworthy. The scam exploits that assumption. The money you received isn't proof of anything except that the scammer has access to a payment method that hasn't been flagged yet.

The request to send it back feels reasonable. Mistakes happen. You've probably sent a text to the wrong person or dialed the wrong number. Sending money to the wrong account seems plausible. The scammer is counting on you to extend the same empathy you'd want if you made that mistake.

The scam also benefits from the social norm of helpfulness. If someone asks for help fixing an error, refusing feels rude. You don't want to be the person who kept money that wasn't theirs. The scammer frames the situation so that doing the right thing means doing what they want.

In The Sting, the con works because the mark believes they're the one running the scam. They think they're cheating the system, so they don't question the setup. The "sent in error" scam uses a similar inversion. You think you're correcting an error. You don't realize you're the target until the money disappears.

The urgency is deliberate. The scammer messages you quickly after the payment arrives. They might send multiple messages if you don't respond immediately. That urgency is designed to prevent you from pausing, thinking, or contacting the platform. The faster you act, the less likely you are to recognize the scam.

What to do when you receive an unexpected payment

If money appears in your account from someone you don't recognize, stop. Don't respond to the sender. Don't send anything back. Contact the platform's support team directly through the app or website.

Every major payment platform has a process for handling erroneous transfers. Venmo, Zelle, and Cash App all allow users to report unexpected payments. The platform can investigate, verify the source, and reverse the transaction if it was genuinely sent in error. That process protects both you and the sender.

If you respond to the sender directly, you're operating outside the platform's protections. You're trusting that the person messaging you is who they claim to be and that their story is accurate. You have no way to verify either of those things. The platform does.

If the sender keeps messaging you, ignore them. Legitimate users who made a real mistake will contact the platform. Scammers will pressure you to act quickly. The difference in behavior is the tell.

If you've already sent money back and you suspect it was a scam, contact the platform immediately. Report the transaction. Explain what happened. Platforms can sometimes freeze the scammer's account or reverse the transfer if you act quickly. The FTC's fraud reporting tool also tracks these scams and helps law enforcement identify patterns.

If the original payment reverses and your account goes negative, contact the platform's support team. Explain the situation. Some platforms will work with you if you were clearly the victim of a scam. Others will hold you responsible for the negative balance because you initiated the return payment. The outcome depends on the platform's policies and how quickly you reported the issue.

Red flags that signal a scam

Certain patterns show up repeatedly in "sent in error" scams. If you see these, stop and verify before doing anything:

The sender messages you immediately after the payment arrives. Legitimate mistakes don't come with instant follow-up messages. Scammers message quickly to catch you before you have time to think.

The sender asks you to send the money back directly rather than going through the platform's support process. Legitimate users know platforms have tools for reversing erroneous payments. Scammers want you to bypass those tools.

The sender creates urgency. They claim they'll face fees, penalties, or account problems if you don't send the money back immediately. Legitimate mistakes don't come with artificial deadlines.

The sender overpaid for a purchase or service and asks you to refund the difference. This is almost always a scam. Legitimate buyers don't overpay and then ask for refunds through separate transactions.

The sender claims they used a business account and need the money back to avoid accounting issues. This is a common excuse designed to add credibility and urgency. It's almost always false.

The payment amount is round and significant. Scammers often send amounts like $500, $1,000, or $2,000 because those figures are large enough to motivate you to respond but not so large that they trigger immediate platform scrutiny.

The sender's account is new or has minimal transaction history. Scammers create accounts specifically for running this fraud. Platforms eventually catch and ban them, so they cycle through new accounts frequently.

Platform-specific risks: Zelle vs. Venmo vs. Cash App

The "sent in error" scam works on all major payment platforms, but the risk profile differs depending on which app the scammer uses.

Zelle transfers are bank-to-bank and nearly instant. Once you send money through Zelle, reversal is difficult. The platform treats Zelle transfers like cash. If you send money back to a scammer through Zelle, you have almost no recourse. The Consumer Financial Protection Bureau has documented cases where Zelle users lost thousands because the platform's fraud protections are weaker than card-based services.

Venmo offers more fraud protection because it's not a direct bank transfer. The platform can freeze accounts, investigate disputes, and reverse transactions. But those protections activate after you've already sent money back. Venmo's social feed also creates a secondary risk: scammers can see who you interact with and use that information to make their messages more convincing.

Cash App operates similarly to Venmo in terms of fraud protection. The platform can investigate and reverse fraudulent transactions, but the process takes time. If you send money back to a scammer through Cash App, you're relying on the platform's willingness to intervene. That intervention isn't guaranteed.

All three platforms have improved their fraud detection in recent years, but the core vulnerability remains: they prioritize speed over verification. That design choice is what makes the "sent in error" scam possible.

What happens to the scammer's account

When a platform identifies a scam account, they freeze it and reverse any pending transactions. But by that point, the scammer has usually already moved the money. They transfer funds out of the platform immediately after you send it back. They might use multiple accounts to obscure the trail. They might convert the money to cryptocurrency or gift cards to make it harder to trace.

Platforms share data about scam accounts with each other and with law enforcement. Repeat offenders get flagged across multiple services. But scammers adapt. They create new accounts. They use stolen identities. They exploit the gap between detection and enforcement.

The FBI's Internet Crime Complaint Center tracks payment app fraud as part of its annual reporting. The 2023 data showed that scams involving peer-to-peer payment platforms cost victims hundreds of millions of dollars. The "sent in error" variant is a growing share of that total because it's simple, scalable, and hard to prevent.

Legitimate accidental transfers do happen

Not every unexpected payment is a scam. People do send money to the wrong account. Usernames on Venmo and Cash App can be similar. Phone numbers get mistyped. Legitimate mistakes happen.

The difference is in how the sender handles it. A legitimate user will contact the platform's support team. They'll follow the official process for reversing the transfer. They won't pressure you to send money back immediately. They won't create urgency. They won't bypass the platform's tools.

If you receive an unexpected payment and you're unsure whether it's legitimate, contact the platform. Let them investigate. If it was a real mistake, the platform will reverse it properly. If it was a scam, you've avoided losing money.

The safest default is to treat every unexpected payment as suspicious until the platform confirms otherwise. That approach might feel overly cautious, but it protects you from a scam that's designed to exploit your willingness to help.

Long-term account security after a scam

If you've been targeted by a "sent in error" scam, even if you didn't lose money, review your account security. Scammers sometimes use this scam as a test to see if you'll respond. If you engage, they know you're a potential target for other scams.

Change your password on the payment app. Enable two-factor authentication if you haven't already. Review your linked bank accounts and cards to make sure nothing was added without your knowledge. Check your transaction history for any unfamiliar activity.

If you did lose money, monitor your bank account and credit reports. Scammers who successfully run one scam sometimes use the same victim for additional fraud. They might try phishing emails, fake customer support calls, or other social engineering attacks.

The FTC's identity theft recovery site provides step-by-step guidance if you suspect your information was compromised. The site walks through credit freezes, fraud alerts, and account monitoring. It's worth reviewing even if you only lost money in the scam and didn't share personal information.

Teaching others to recognize this scam

The "sent in error" scam works partly because it's not widely known. People understand phishing emails and fake tech support calls. They're less familiar with scams that start with receiving money.

If someone you know uses Venmo, Zelle, or Cash App, talk to them about this scam. Explain the mechanism. Walk through what an unexpected payment looks like and what to do if it happens. The conversation takes five minutes and might prevent someone from losing hundreds of dollars.

The scam is particularly effective against people who are new to payment apps or who use them infrequently. They're less familiar with the platform's fraud protections. They're more likely to trust a message that seems reasonable. A brief explanation of how the scam works can shift their default response from "send it back" to "contact support."

The platforms themselves have started adding warnings and educational content, but user awareness is still the strongest defense. Scammers rely on the gap between what the platform knows and what users know. Closing that gap makes the scam harder to execute.